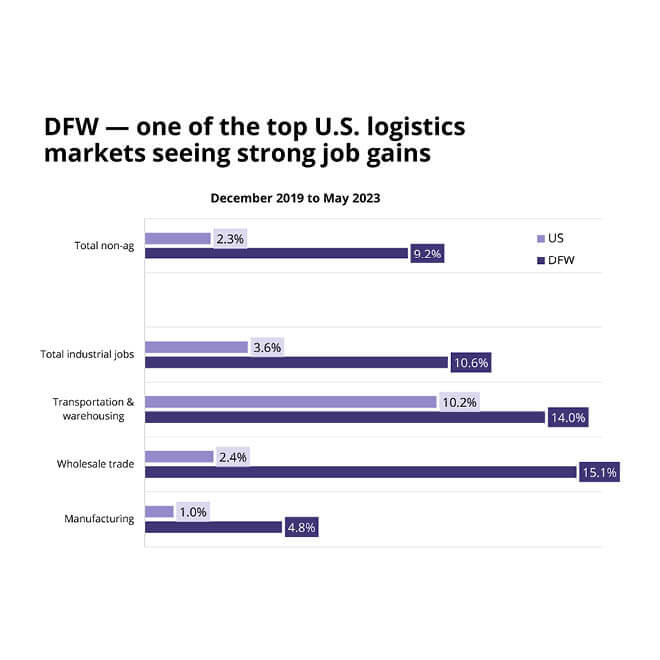

Throughout 2023, industrial has continued to be the CRE belle of the ball, with Dallas-Fort Worth (DFW) and Austin serving as industrial activity hubs. The Avison Young Q2 ‘23 Dallas-Fort Worth Industrial Market Report stated that 78,000 industrial industry jobs have been added throughout the DFW Metroplex since the end of 2019.

This 10.6% growth is three times the U.S. average. DFW added 27,000 industrial jobs in just the previous year, according to the report. This is good news for DFW and Texas as a whole.

This growth further shows why DFW continues to lead the nation as a strong logistics hub, often credited to its affordability, central location and two major airports, along with a key cargo airport in Fort Worth’s Alliance Airport.

As good as the industrial market is, especially here in DFW and Texas, steadily rising interest rates continue to dampen construction starts, which have been decreasing since late 2022. Less new construction inventory may mitigate or reverse the national decline in rent growth and eventually stabilize the current vacancy expansion, according to Q2 CRE market data from Baker Tilly, a leading advisory tax and assurance firm.

Additionally, Avison Young notes an 8.1% increase in vacancy rates across DFW. A recent CoStar article shared how more industrial buildings are entering the DFW market with 45M SF being completed so far this year, the highest on record. In fact, this accounts for 14% of completed space across the U.S. That’s a lot of space available and waiting for tenants.

A more concerning trend is the rate at which rents have been rising. Avison Young states that DFW rents have increased 18.7% in the last year alone, with the average being $6.98 per square foot. These higher rents are also fueling higher acquisition and development costs.

From a construction standpoint, this price escalation makes sense, as material prices are still elevated from the COVID-19 pandemic and resulting shutdown. In 2021, we saw unprecedented construction costs, with lumber and steel being the highest recorded through available government data since 1949. Lately, we have seen costs revert to the standard 4 to 5% price increase so they are trending in the right direction, but it will take a while to recover from such spikes.

DFW’s strength as a premier distribution hub continues despite these escalating rents because the region remains one of the most affordable logistics centers in the U.S.

Other areas of Texas are also experiencing upward industrial real estate trends. The Baker Tilly data shows how Austin has seen sustained industrial demand. Though this is bolstered by big names like Tesla and Samsung building factories in and around Texas’ capital, they have in turn attracted additional ancillary manufacturers, suppliers and third-party logistics providers.

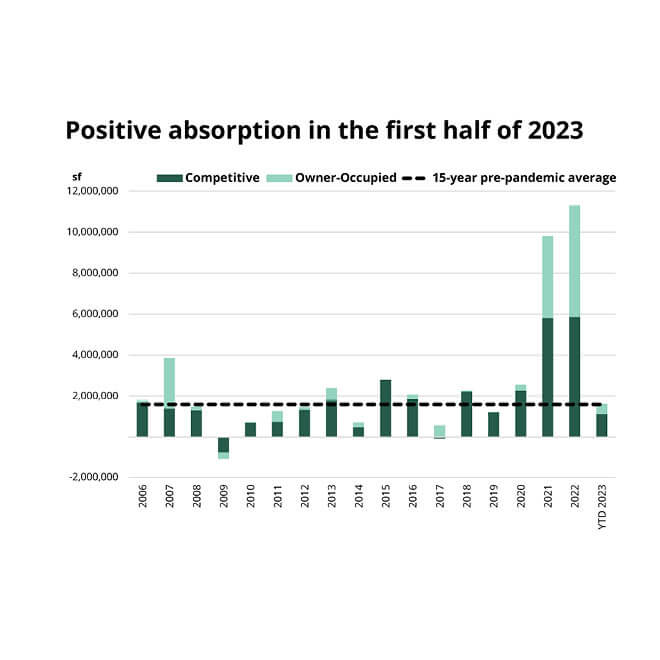

Austin’s industrial market continues to demonstrate remarkable resilience and strength despite economic uncertainty. Another Avison Young industrial market report says Austin saw a notable 1M SF of positive absorption in Q2, which is an 81.5% jump from Q1. In total, 1.6M SF have had positive absorption in the first two quarters, surpassing pre-pandemic averages showcasing a healthy and active industrial market.

AP is working on several industrial facilities. Most notably, we are currently constructing IDI Logistics’ Sunrise Commerce Center in Round Rock, just north of Austin. The Class A industrial development will consist of five speculative buildings totaling more than 465k SF across two phases. AP will construct the buildings and perform tenant finishes. The project is planned for completion in late 2023.

AP is also part of an industrial project in the DFW Metroplex that will contain five structures totaling 908k SF of core and shell distribution buildings. Construction is anticipated to be completed by Summer 2024.

As an engaged industrial construction partner, we predict sustained demand and growth in industrial construction in both regions, with a specific emphasis in Central Texas. This is enhanced by the influx of people moving to Austin in the previous year. A recent Cushman-Wakefield report states a whopping 51,000 industrial jobs were added in the Austin market in the previous 12 months.

As 2023 rounds third and heads for home, it will be interesting to see how these trends persist. I believe we will continue to see industrial real estate grow across North and Central Texas. Even if rent rates continue to climb, which they likely will due to demand, cost and interest rates, industrial facilities are and will continue to be needed. With their prime location and low cost, I see North and Central Texas continuing to serve as industrial hubs. We will see what 2024 brings.

As Vice President of Preconstruction and Estimating, Granger Hassmann leads the region’s preconstruction and estimating departments. His responsibilities include the development of preconstruction strategies on large, complex and high-risk projects while ensuring alignment with the client’s strategic goals. He is responsible for developing an environment of accountability to ensure that the preconstruction department performance is consistent with project planning, scope and budget.

Sunrise Commerce Center, AP’s Central Texas industrial project.

Sunrise Commerce Center, AP’s Central Texas industrial project.